In another record year for wind power, at least 44 countries added a combined 45 GW of wind energy capacity (more than any other renewable technology), increasing the global total by 19% to 283 GW.

The United States was the leading market, but China remains the leader for total installed capacity. Wind power is expanding to new markets, aided by falling prices.

Almost 1.3 GW of capacity was added offshore wind energy (mostly in northern Europe), bringing the total to 5.4 GW in 13 countries.

The wind energy industry has been challenged by downward pressure on prices, combined with increased competition among turbine manufacturers, competition with low-cost gas in some markets, and reductions in policy support driven by economic austerity.

During 2012, almost 45 GW of wind power capacity began operation, increasing global wind capacity 19% to almost 283 GW. It was another record year for wind power, which again added more capacity than any other renewable technology despite policy uncertainty in key markets.

The top 10 countries accounted for more than 85% of year-end global capacity, but the market continued to broaden.

Around 44 countries added capacity during 2012, at least 64 had more than 10 MW of reported capacity by year’s end, and 24 had more than 1 GW in operation. From the end

of 2007 through 2012, annual growth rates of cumulative wind power capacity averaged 25%.

of 2007 through 2012, annual growth rates of cumulative wind power capacity averaged 25%.

For the first time since 2009, the majority of new capacity was installed in the OECD, due largely to the United States. Developing and emerging economies are moving firmly into the mainstream, however. The United States and China together accounted for nearly 60% of the global market in 2012, followed distantly by Germany, India, and the United Kingdom.

Others in the top 10 for capacity added were Italy, Spain, Brazil, Canada and Romania. The EU represented about 27% of the world market and accounted for just over 37% of total global capacity (down from 40% in 2011).

The United States had its strongest year yet and was the world’s top market in 2012. U.S. wind farm installations nearly doubled relative to 2011, with almost 64% of the 13.1 GW added coming on line in the year’s final quarter. The strong market was driven by several factors including increased domestic manufacturing of turbine parts and technology improvements that are increasing efficiency and driving down costs; most important, however, was the expected expiration of the federal Production Tax Credit.

Wind power represented as much as 45% of all new electric generating capacity in the United States, outdoing natural gas for the first time, and the 60 GW operating at year’s end was enough to power the equivalent of 15.2 million U.S. homes.

The leading states for capacity added were Texas (1.8 GW), with more than 12 GW in operation, California (1.7 GW), and Kansas (1.4 GW), and 15 states had more than 1 GW in operation by year’s end.

China installed almost 13 GW, accounting for 27% of the world market, but showed a significant decline in installations and market share relative to 2009–2011.

The market slowed largely in response to stricter approval procedures for new projects to address quality, safety, and grid access concerns. Another major constraint has been the high rate of curtailment—averaging 16% in 2011—which results when output temporarily exceeds the capacity of the transmission grid to transfer wind power to demand centres.

Even so, at year’s end China had nearly 75.3 GW of wind energy capacity; as in 2010 and 2011, about 15 GW of this total had not been commercially certified by year-end, although most was feeding electricity into the grid.

Wind generated 100.4 billion kWh in 2012, up 37% over 2011 and exceeding nuclear generation for the first time. By year’s end, almost 25% of total capacity was in the Inner Mongolia Autonomous Region, followed by Hebei (10.6%), Gansu (8.6%), and Liaoning (8.1%) provinces, but wind is spreading across China—nine provinces had more than 3 GW of capacity each, and 14 had more than 1 GW each.

The European Union passed the 100 GW milestone in 2012, adding a record 11.9 GW of wind capacity for a total exceeding 106 GW. Wind power came in second for electric capacity added (26.5%), behind solar PV (37%) and ahead of natural gas (23%); by year’s end, wind accounted for 11.4% of total EU electric capacity.

Despite record growth, there is concern that the EU lags on its National Renewable Energy Action Plan (NREAP) targets, and that 2012 additions do not reflect growing economic and policy uncertainty (most capacity was previously permitted and financed). Some emerging markets are poised for significant growth, but grid connectivity and economic issues pose challenges to future development in much of Europe, as do land issues arising from having so much capacity on shore.

Germany remained Europe’s largest market, rebounding strongly with its highest installations in a decade (2.4 GW), for a total of 31.3 GW.

The United Kingdom ranked second for new installations in Europe for the second year running, adding 1.9 GW (45% offshore) for more than 8.4 GW by year’s end; it now ranks third regionally for total capacity, behind Germany and Spain, and sixth globally.26 Italy (1.3 GW), Spain (1.1 GW), Romania (0.9 GW), and Poland (almost 0.9 GW) were the other leading markets in Europe.

Romania and Poland both had record years, with Poland’s total capacity up nearly 55% and Romania’s almost doubling.

India added about 2.3 GW to maintain its fifth-place ranking with a total of 18.4 GW at year’s end.29 India’s most important federal wind power incentives were suspended or reduced inearly 2012; despite strong policies in many states, uncertainty at the national level affected investment decisions and slowed markets.

Although there was a slowdown in both China and India, Asia remained the largest market for the fourth year in a row, adding a total of 15.5 GW in 2012, compared with North America’s 14.1 GW and all of Europe’s 12.2 GW.

Elsewhere, the most significant growth was seen in Latin America. Brazil added 1.1 GW to rank eighth globally for newly installed capacity, and it ended 2012 with enough capacity (2.5 GW) to meet the electricity needs of 4 million households.

Brazil’s electric grid is not expanding as rapidly as its wind capacity, however, slowing the ability to get new wind power online.

Mexico also had a strong year, adding 0.8 GW to approach 1.4 GW total, and brought the region’s largest project (306 MW) on line. Others in the region to add capacity included Argentina, Costa Rica, Nicaragua, Uruguay, and Venezuela, which commissioned its first commercial wind farm (30 MW).

To the north, Canada had its second best year, adding more than 0.9 GW for a total of 6.2 GW. Three provinces reached milestones, with Ontario passing 2 GW total and Alberta and Quebec achieving 1 GW each.

Africa and the Middle East saw little development, but Tunisia almost doubled its capacity, adding 50 MW; Ethiopia joined the list of countries with commercial-scale wind farms, installing 52 MW; and construction began on several South African projects totaling more than 0.5 GW.

Elsewhere, Turkey added 0.5 GW for a total of 2.3 GW, and Australia was the only country in the Pacific to add capacity (0.4 GW), bringing its total to nearly 2.6 GW.

Worldwide, 13 countries had wind turbines operating offshore by the end of 2012, with 1.3 GW added for a total of 5.4 GW. More than 90% of this capacity was located off northern Europe, which continued to lead in offshore wind farm developments, adding a record 1.2 GW (up 35% over 2011) for almost 5 GW total in 10 countries.40 The United Kingdom accounted for 73% of Europe’s additions, due largely to completion of the first phase of the London Array (630 MW), the world’s largest offshore wind farm; the U.K. ended 2012 with more than 2.9 GW offshore, followed in Europe by Denmark (0.9 GW), Belgium (0.4 GW), and Germany (0.3 GW).

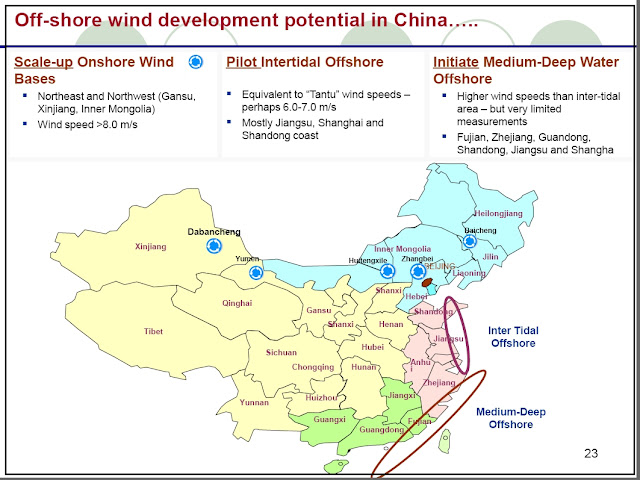

The remaining offshore capacity was in China (0.4 GW), Japan (25.3 MW), and South Korea (5 MW), which added 127 MW, 0.1 MW, and 3 MW, respectively.

The trend towards increasing size of individual projects continued, driven mainly by cost considerations. Europe’s largest onshore wind farm (600 MW) was connected to the grid in Romania, and the largest U.S. wind farm (845 MW), which began operating in Oregon, is expected to power 235,000 U.S. homes.

Independent power producers and energy utilities are currently the most important clients in the market in terms of capacity installed, but interest in community-owned wind power projects is rising in Australia, Canada, Japan, the United States, parts of Europe, and elsewhere. In the U.S. state of Iowa alone, at least six community projects came on line in 2012, and several projects were under way in Australia by year’s end.

In Japan, interest has increased considerably since the Fukushima disaster in March 2011. Community power represents the mainstream ownership model in Denmark and Germany.

The use of small-scale wind turbines is also increasing to meet energy needs both on- and off-grid and is driven by the development of lower-cost grid-connected inverters; volatile or rising fossil fuel prices; and government incentives.

Off-grid and mini-grid uses prevail, particularly in China and other developing countries. Applications are expanding and include rural electrification, water pumping, telecommunications, defence, and other remote uses. There are two distinct markets: models with rated capacity below 10 kW, and those in the 10–500 kW range.

In general, the market is evolving towards 50 kW and larger turbines because they are easier to finance.

Worldwide, at least 730,000 small-scale turbines were operating at the end of 2011, totaling 576 MW (up 27% over 2010). China accounts for 40% of global capacity and the United States for 35%, followed by the United Kingdom (11%), Germany (2.6%), Ukraine, Canada, Italy, Poland, and Spain.

In 2012, the total capacity of U.S. sales of small-scale wind turbines was 18.4 MW. With the exception of China, most interest is in North America and Europe, with slow progress in emerging wind energy markets.

Total wind power capacity by the end of 2012 was enough to meet at least 2.6–3% of global electricity consumption. In the EU, wind capacity operating at year’s end was enough to cover 7% of the region’s electricity consumption in a normal wind year (up from 6.3% in 2011).

Several countries met higher shares of their electricity demand with wind, including Denmark (30% in 2012; up from nearly 26% in 2011), Portugal (20%; up from 18%), Spain (16.3%; up from 15.9%), Ireland (12.7%, up from 12%), and Germany (7.7%; down from 8.1%).

Four German states had enough capacity at year’s end to meet over 49% of their electricity needs with wind, and through the month of July the state of South Australia generated 26% of its electricity with wind power.

In the United States, wind power represented 3.5% of total electricity generation (up from 2.9% in 2011) and met more than 10% of demand in nine states (five in 2011), with Iowa nearing 25% (up from 19%) and South Dakota at 24% (up from 22%).

During 2005–2009, wind turbine prices increased in response to growing global demand, rising material costs, and other factors; since then, however, growing scale and greater efficiency have combined to improve capacity factors and reduce costs of wind turbines as well as operations and maintenance.

During 2005–2009, wind turbine prices increased in response to growing global demand, rising material costs, and other factors; since then, however, growing scale and greater efficiency have combined to improve capacity factors and reduce costs of wind turbines as well as operations and maintenance.

Oversupply in global turbine markets has further reduced prices, benefitting developers by improving the cost-competitiveness of wind power relative to fossil fuels. However, the industry has been challenged by downward pressure on prices, combined with increased competition among turbine manufacturers, competition with low-cost gas in some markets, and reductions in policy support driven by economic austerity.

Relative to their 2008 peak, turbine prices fell by as much as 20–25% in western markets and more than 35% in China before stabilising in 2012. The costs of operating and maintaining wind farms also dropped significantly due to increased competition among contractors and improved turbine performance.

As a result, onshore wind-generated power is now cost-competitive with or cheaper than conventional power in some markets on a per kilowatt-hour basis (including some locations in Australia, India, and the United States), although new shale gas in some countries is making it more difficult for wind (and other renewables) to compete with natural gas.

Offshore wind energy remains at least twice as expensive as onshore.

The world’s top 10 turbine manufacturers captured 77% of the global market and, as in 2011, they hailed from China (4), Europe (4), India (1), and the United States (1).

Vestas (Denmark), the top manufacturer since 2000, surrendered its lead to GE Wind (third in 2011), which blew ahead due mainly to the strong U.S. market. Siemens moved from ninth to third, followed by Enercon (Germany) and Suzlon Group (India), both of which moved up one spot relative to 2011.

Other top companies were Gamesa (Spain) and Goldwind, United Power, Sinovel, and Mingyang (all China); both Goldwind and Gamesa dropped out of the top five.

In 2012, more than 550 manufacturing facilities were making wind turbine components in every region of the United States; despite ongoing policy uncertainty, the share of equipment

produced domestically increased considerably over the past decade, reducing transport-related costs and creating jobs.

produced domestically increased considerably over the past decade, reducing transport-related costs and creating jobs.

In Europe, industry activity focused increasingly on offshore technologies and project development in Eastern Europe and other emerging markets. By late 2012, Brazil was home to 11 manufacturing plants and GE had a facility under construction, and India had 19 manufacturers with a consolidated annual production capacity exceeding 9.5 GW.

In general, however, the turbine manufacturing industry was hit hard by rising costs, reductions in government support, and overcapacity, with several manufacturers delaying or cancelling expansion plans, scaling back operations, reducing their workforce, or filing for bankruptcy 75 In the United States, companies throughout the wind energy supply chain reduced workforces and closed facilities due to policy uncertainty.

Vestas (Denmark) chose to restructure, let go of thousands of employees, and end production of its kW size machines.

Sinovel (China) put workers on leave, and many suppliers in China in particular have been pushed to the edge of collapse, with overcapacity pushing smaller manufacturers out of the market.

Suzlon (India) has lost money for three years running and has struggled with massive debt.

At the same time, expansion and innovation continued in 2012. Local-content requirements have not only spawned trade disputes but also led turbine manufacturers to build factories close to growing markets for competitive advantage.

Chinese companies are taking package deals (including government-backed loans) to emerging markets and are establishing subsidiaries and partnerships with local companies to deploy their excess capacity.

Manufacturers are also assuming more risk to increase their share of the growing market for turbine maintenance, which is expected to provide relatively stable margins. Turbine designs continue to evolve in order to reduce costs and/or improve performance, with trends towards longer blades, lower wind speeds, and new materials such as concrete for towers and carbon fibre for blades.

At least two companies launched wind turbines for low-wind sites in 2012, and GE started developing blades made of tough, flexible fabric that could reduce blade costs by 25–40%. There is also a shift forwards towards automated manufacturing of blades and a shift back to traditional doubly-fed induction generators and medium-speed hybrid drives.

The trend towards ever-larger wind turbines continued in 2012, with the average size delivered to market rising to 1.8 MW (from 1.7 GW in 2011). Average wind turbine sizes were 3.1 MW in Denmark, 2.4 MW in Germany, 1.9 MW in the United States, 1.6 MW in China, and 1.2 MW in India.

During 2012, the average size installed offshore in Europe was up 14% over 2011 to 4 MW, and 31 companies announced plans for 38 new offshore turbine models, with three-quarters of these being 5 MW and up.

Most manufacturers are developing wind turbines in the 4.5–7.5 MW range, with 7.5 MW being the largest size that is commercially available, but several companies announced plans in 2012 to develop even larger machines.

Wind turbines are also rising higher and being outfitted with longer blades to capture more energy: REpower erected its tallest turbine to date, with a 143-metre hub height, and Siemens unveiled the “longest blades in the world” at 75 metres.

In addition to seeing larger wind turbines, the offshore wind industry is moving into deeper water, farther from shore, and with greater total capacities per project, leading to increased interest in floating platforms.

Several countries have pilot programmes for floating wind turbines, and Japan launched its first (100 kW machine) in 2012, with plans to install a full-scale machine in 2013. In Europe, the average offshore wind farm size increased 36% relative to 2011 (to 271 MW).

As offshore projects become larger, there is growing competition for manufacturing capacity and installation resources, creating a trend towards vertical integration and consolidation in the supply chain, including installation vessels, with several project developers securing vessels and some funding new ones.

The small-scale (<100 kW) wind industry also continued to mature in 2012, with hundreds of manufacturers worldwide, expanding dealer networks, and increasing importance of turbine certification.

Most manufacturers and service providers are concentrated in China, North America, and Europe. As an example of efforts to diversify to survive, RRB Energy Ltd. of India is restarting production of a slightly larger-scale 225 kW turbine, discontinued in 2005, with plans to export many of the units to emerging markets in Africa and elsewhere. Gamesa plans to move into development of distributed and community wind projects.