With about 37,007 megawatts (MW) of solar photovoltaic PV power installed in 2013, world solar PV power capacity increased about 35% to 136,697 MW. Whereas Europe had dominated annual growth for years up until 2013 (10 years, to be precise), solar PV growth was much more evenly split last year, and China actually topped the tables.

“While Europe concentrated more than 70% of the world’s new PV installations in 2011 and still around 59% a year later, with more than 10 GW of new capacity installed in 2013, Europe only accounted for 28% of the world’s market.”

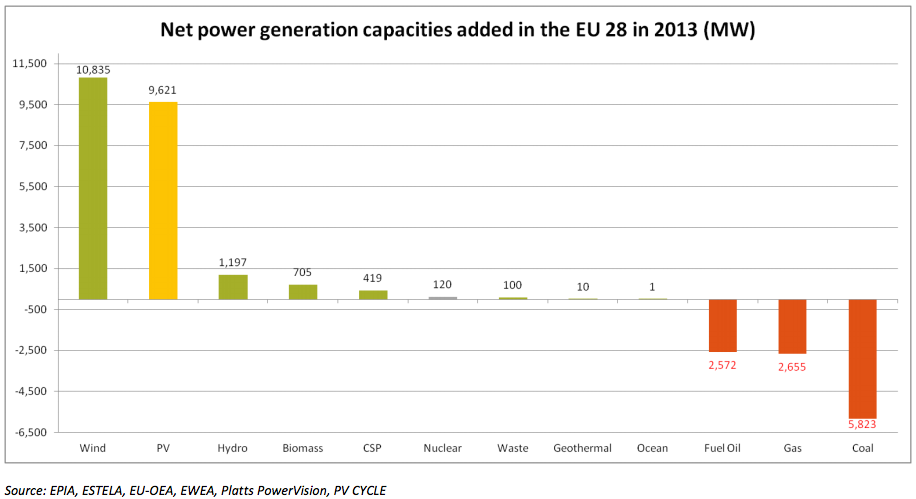

Nonetheless, Europe still saw fairly large growth in solar PV capacity, especially when you compare that to most other energy sources. Here’s a chart showing net generation capacity change in the EU 28 for various energy sources.

Aside from being the #2 source of new electricity generation capacity in 2013, solar PV now accounts for about 3% of electricity demand in Europe and about 6% of peak electricity demand (remember that solar panels provide electricity in the daytime, when electricity demand is higher).

Nonetheless, there’s no denying the EU market was not nearly as strong in 2013 as in previous years. Austerity measures have been especially harmful. EPIA notes: “European PV markets have experienced a slowdown. In a number of European countries, this can be explained by harmful and retrospective measures that have badly affected investors’ confidence and PV investments viability. Italy in particular experienced a 70% market decrease compared to the year before. Germany also experienced in 2013 a steep PV market decrease (57% decrease compared to 2012).”

Note that these aren’t final numbers. “EPIA will publish in June 2014 consolidated and detailed historical figures and forecasts in its ‘Global Market Outlook for Photovoltaics 2014-2018′ report,” the preliminary report states.

Nonetheless, it was definitely a record year. 37,007 MW is a big step above 29,865 MW and 30,282 MW (the totals for 2012 and 2011, respectively).

Here are some other notes from the EPIA preliminary report:

Top 3 global countries

- China was the n°1 global market with around 11.3 GW connected to the grid.

- With around 6.9 GW, Japan was the second global biggest market in 2013.

- The US ranked n°3 with 4.8 GW.

Evolution of European markets

- Germany was the top European market with 3.3 GW (down from 7.6 GW in 2012).

- Several European markets were close to the gigawatt mark: Italy (between 1.1 GW and 1.4 GW), UK (in between 1 GW and 1.2 GW), Romania (1.1 GW) and Greece (1.04 GW).

- Other European markets that performed well in the past went significantly down in 2013, resulting from political decisions aimed at reducing the level of support to PV: Belgium (from 600 MW in 2012 to 215 MW in 2013), France (from 1.1 GW to 613 MW), Denmark (from 300 MW to around 200 MW).

- Over the last three years however, outside Germany and Italy, the size of the European PV market has been relatively stable, at around 6 GW per year, thanks to the growth in some countries that has balanced the decline in others.

- Some markets in Europe have an almost untapped PV potential, Hungary, Poland and Turkey for instance. The PV potential in countries like France and Spain is still largely unexploited.

Evolution of Asian markets

- China and Japan have led the dynamism of the Asian PV market (with respectively around 11.3 GW and 6.9 GW).

- Several Asian markets continued to grow at a moderate pace: India (1.1 GW), Korea (442 MW), Thailand (317 MW).

![An American Tail [1986] [DVD5-R1] [Latino]](http://iili.io/FjktrS2.jpg)