The global PV industry's recent past has seen wafer, cell, and module suppliers at the mercy of an inhospitable supply-demand imbalance throughout the global market.

FIGURE: Contribution of Key Drivers Toward Module Cost Reduction, Best-in-Class China Producer, Q4 2010-Q4 2012

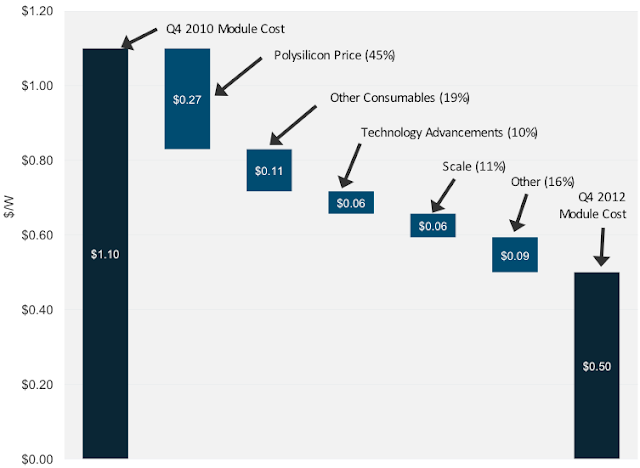

Source: PV Technology and Cost Outlook, 2013-2017

With supply consistently 200% of demand annually, c-Si module prices have fallen approximately 70% in two years. One positive externality of this cutthroat pricing is that manufacturing costs have fallen in line with pricing declines. This is mostly because pricing for key inputs further up the value chain has also fallen as a result of overcapacity and consequent margin evaporation.

Back in 2009/10, industry roadmaps were targeting $1.00/W module costs as a medium-term goal. With best-in-class Chinese producers approaching costs of $0.50/W in 2013, yesterday’s goals are no longer relevant today. However, as noted, the majority of cost reduction over the last two years has been driven by declines in consumables prices. This state of affairs has left both manufacturers and their customers with considerable uncertainty, and there is currently little consensus on what is a realistic goal for the module supply chain to set for itself over the next three to five years. It is in the context of this lack of clarity that this report was conceived.

Source: PV Technology and Cost Outlook, 2013-2017

With supply consistently 200% of demand annually, c-Si module prices have fallen approximately 70% in two years. One positive externality of this cutthroat pricing is that manufacturing costs have fallen in line with pricing declines. This is mostly because pricing for key inputs further up the value chain has also fallen as a result of overcapacity and consequent margin evaporation.

Back in 2009/10, industry roadmaps were targeting $1.00/W module costs as a medium-term goal. With best-in-class Chinese producers approaching costs of $0.50/W in 2013, yesterday’s goals are no longer relevant today. However, as noted, the majority of cost reduction over the last two years has been driven by declines in consumables prices. This state of affairs has left both manufacturers and their customers with considerable uncertainty, and there is currently little consensus on what is a realistic goal for the module supply chain to set for itself over the next three to five years. It is in the context of this lack of clarity that this report was conceived.

This 112-page report on the latest in c-Si PV wafer, cell, module, and materials technology is the most recent analysis from GTM Research's flagship supply-side practice, and aims to provide a competitive outlook on the leading technology and cost trends through 2017 across the global PV supply chain. The report explores existing and innovative technology advancements in ingot growth, wafer slicing, cell processing, and module assembly, as well as their impacts on efficiencies and manufacturing costs.

The report then presents GTM's proprietary cost model through 2017 for polysilicon, wafer, cell and modules. Details on our cost model and forecast are below.

The report then presents GTM's proprietary cost model through 2017 for polysilicon, wafer, cell and modules. Details on our cost model and forecast are below.

REPORT SCOPE: COST FORECAST MODELING

- Goal: The goal of this new report is to provide a quantitative understanding of crystalline silicon PV manufacturing costs that is both comprehensive and granular. Rather than estimating costs across a variety of regions, technologies and producer profiles– as is done on a monthly basis in our Global PV Competitive Intelligence Tracker– the goal here is to focus on costs attained by best-in-class (meaning lowest-cost) China-based producers for benchmarking purposes. Examples of such producers would be Jinko Solar, Renesola, Trina Solar and Yingli Green Energy.

- Time Period: Detailed cost breakdowns are estimated annually for the fourth quarter from 2011 to 2017.

- Cost Elements: The cost centers covered in this report include the following: depreciation, materials/consumables, labor, utilities, and overhead (plant and property).

- Technology Modeling: Manufacturing costs are estimated separately for monocrystalline and multicrystalline producers. Technology modeling assumes the incorporation of two advanced technology platforms– diamond wire sawing (wafer) and selective emitter (cell)– for assumed best-in-class mono producers from 2012 and 2013 onwards, respectively. Aside from this, the report assumes a fairly standard device architecture and process flow for ingot fabrication through module assembly in cost modeling.

- Variance Analysis: Given the number of variables that affect module manufacturing cost structure and the uncertainty surrounding their future behavior (e.g., consumables pricing, manufacturer scale, technology parameters), the report supplements base-case cost forecasts with high- and low-case forecasts to place realistic upper and lower bounds on best-in-class module costs over the next five years.

FIGURE: Data Sources Consulted for Key Inputs![]()