Annual wind power additions in the U.S. achieved record levels in 2012, while wind energy pricing is near an all-time low, according to a new report released by the U.S. Dept. of Energy (DOE) and prepared by Lawrence Berkeley National Laboratory (Berkeley Lab).

![]()

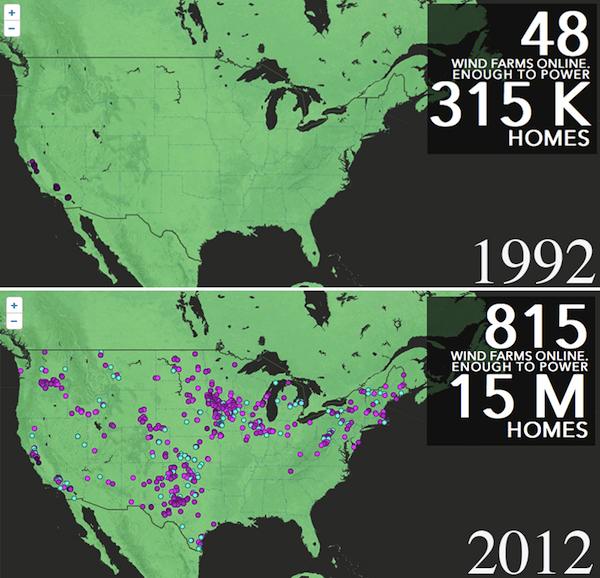

Roughly 13.1 GW of new wind power capacity were connected to the U.S. grid in 2012, well above the previous high in 2009, and motivated by the scheduled expiration of federal tax incentives at the end of 2012.

![]()

The prices offered by wind projects to utility purchasers averaged $40/MWh for projects negotiating contracts 2011 and 2012, spurring demand for wind energy. At the same time, even with a short-term extension of federal tax incentives now in place, the wind power industry is facing uncertain times, in part due to low natural gas prices and continued policy uncertainty.

![]()

“Wind energy prices—particularly in the central U.S.— now rival the lows set back in 2003,” notes Berkeley Lab Staff Scientist Ryan Wiser. “This is especially notable because technology advancements have allowed wind projects to be built in lower quality wind resource areas.”

![]()

Key findings from the DOE’s “2012 Wind Technologies Market Report” include:

http://emp.lbl.gov/sites/all/files/lbnl-6356e.pdf

Roughly 13.1 GW of new wind power capacity were connected to the U.S. grid in 2012, well above the previous high in 2009, and motivated by the scheduled expiration of federal tax incentives at the end of 2012.

The prices offered by wind projects to utility purchasers averaged $40/MWh for projects negotiating contracts 2011 and 2012, spurring demand for wind energy. At the same time, even with a short-term extension of federal tax incentives now in place, the wind power industry is facing uncertain times, in part due to low natural gas prices and continued policy uncertainty.

“Wind energy prices—particularly in the central U.S.— now rival the lows set back in 2003,” notes Berkeley Lab Staff Scientist Ryan Wiser. “This is especially notable because technology advancements have allowed wind projects to be built in lower quality wind resource areas.”

Key findings from the DOE’s “2012 Wind Technologies Market Report” include:

- Wind is a credible source of new generation in the U.S. Wind power comprised 43% of all new U.S. electric capacity additions in 2012 and represented $25 billion in new investment. Wind power currently contributes more than 12% of total electricity generation in nine states (with three of these states above 20%), and provides more than 4% of total U.S. electricity supply.

- Despite challenges, a growing percentage of the equipment used in U.S. wind power projects has been sourced domestically in recent years. Wind turbine and component manufacturers met the challenge of supplying a 13-GW market in 2012, albeit with growing pains. Seven of the ten wind turbine suppliers with the largest share of the U.S. market in 2012 had one or more operational manufacturing facility in the U.S. in 2012; in contrast, only eight years earlier, there was only one active utility-scale turbine manufacturer assembling turbines domestically. In part as a result, a growing percentage of the equipment used in wind projects has been sourced domestically. Focusing on selected trade categories, the percentage of wind turbine costs attributable to imported equipment declined from 75% in 2006-2007 to 28% in 2012. Conversely, if one assumes that no wind equipment imports occurred though other trade categories beyond those analyzed in the report, then domestic content increased from 25% in 2006-2007 to 72% in 2012. Exports of wind-powered generating sets from the U.S. have also increased, rising from $16 million in 2007 to $388 million in 2012.

- Turbine scaling is boosting wind project performance. Since 1998-99, the average nameplate capacity of wind turbines installed in the U.S. has increased by 170% (to 1.94 MW in 2012), the average turbine hub height has increased by 50% (to 84 m), and the average rotor diameter has increased by 96% (to 94 m). This substantial scaling has enabled wind project developers to economically build projects in lower wind-speed sites, and is driving capacity factors higher for projects located in fixed wind resource regimes. Wind power curtailment—disallowing the production of electricity from wind projects even when the wind resource would allow for such production, due to transmission or power system limitations—has recently declined in what have historically been the most problematic areas (e.g., West Texas) as a result of concrete steps taken to address the issue.

- Falling wind turbine prices are pushing installed project costs lower. Wind turbine prices have fallen 20 to 35% from their highs back in 2008, and these declines are pushing project-level costs down. Based on a large sample of wind projects, average project costs in 2012 were down almost $200/kW from the reported average cost in 2011, and down almost $300/kW from the reported average cost in both 2009 and 2010. Among projects built in 2012, the windy Interior region of the country was the lowest-cost region, with average project costs of ~$1,760/kW.

- Wind energy prices have been falling since 2009, and now rival previous lows. Lower wind turbine prices and installed project costs, along with improved capacity factors, are enabling aggressive wind power pricing. After topping out at nearly $70/MWh in 2009, the average levelized long-term price from wind power sales agreements signed in 2011/2012—many of which were for projects built in 2012—fell to around $40/MWh nationwide. This level approaches previous lows set back in the 2000-2005 period, which is notable given that wind projects have increasingly been sited in lower-quality wind resource areas. Wind energy prices negotiated in 2011 and 2012 are generally lowest in the Interior region of the U.S., with prices averaging just above $30/MWh, and typically ranging from $20-40/MWh. Even with today’s very attractive wind energy prices, however, wind power sometimes struggles to compete with what are currently very low natural gas and wholesale power prices in many parts of the country.

- Looking ahead, projections are for slow growth in 2013, followed by a much stronger year in 2014. Though federal tax incentives are now available for wind projects that initiate construction by the end of 2013, it will take time to recharge the project pipeline. “As a result, 2013 is expected to be a slow year for new capacity additions, lowering not only U.S. but global growth forecasts,” says Mark Bolinger, research scientist at Berkeley Lab. “The year 2014, on the other hand, is expected to be a strong year as developers commission projects that began construction in 2013.” Projections for 2015 and beyond are much less certain: despite the improved cost, performance, and price of wind energy, policy uncertainty—in concert with continued low natural gas prices and modest electricity demand growth—may put a damper on medium-term growth expectations.

http://emp.lbl.gov/sites/all/files/lbnl-6356e.pdf