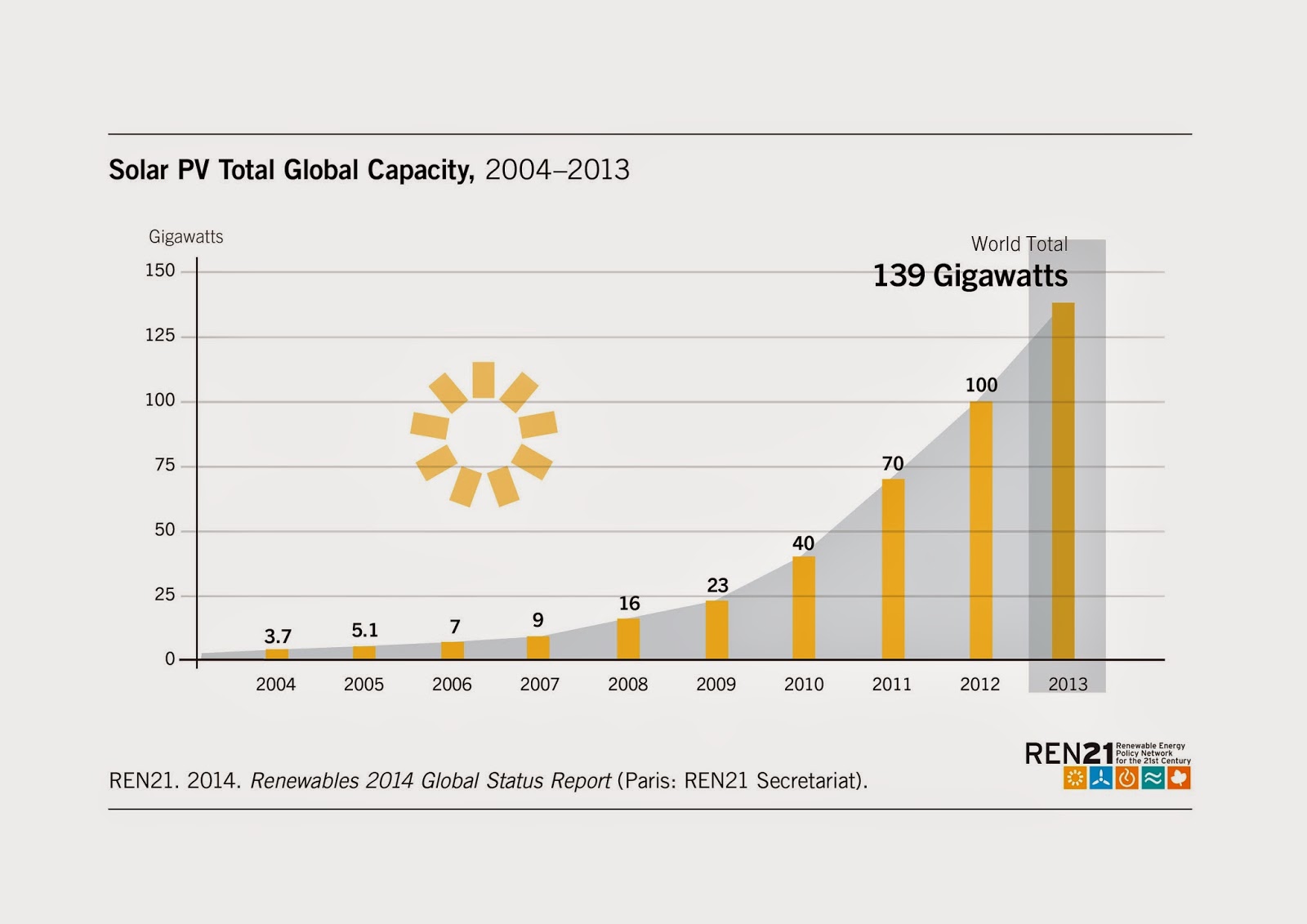

The solar energy photovoltaic PV market had a record year, adding more than 39 GW in 2013 for a total exceeding 139 GW. China saw spectacular growth, accounting for nearly one-third of global capacity added, followed by Japan and the United States.

Solar PV is starting to play a substantial role in electricity generation in some countries, particularly in Europe, while lower prices are opening new markets from Africa and the Middle East to Asia and Latin America. Interest continued to grow in corporate- and community-owned systems, while the number and size of utility-scale systems continued to increase.

Although it was a challenging year for many companies, predominantly in Europe, the industry began to recover during 2013. Module prices stabilised, while production costs continued to fall and solar cell efficiencies increased steadily. Many manufacturers began expanding production capacity to meet expected further growth in demand.

The year saw a major shift geographically as China, Japan, and the United States became the top three installers, and as Asia passed Europe—the market leader for a decade—to become the largest regional market.

China’s spectacular growth offset Europe’s significant market decline, and hid slower-thanexpected

development in the United States and other promising markets.

development in the United States and other promising markets.

Nine countries added more than 1 GW of solar PV to their grids, and the distribution of new installations continued to broaden. By year’s end, 5 countries had at least 10 GW of total capacity, up from 2 countries in 2012, and 17 had at least 1 GW.

The leaders for solar PV per inhabitant were Germany, Italy, Belgium, Greece, the Czech Republic, and Australia.

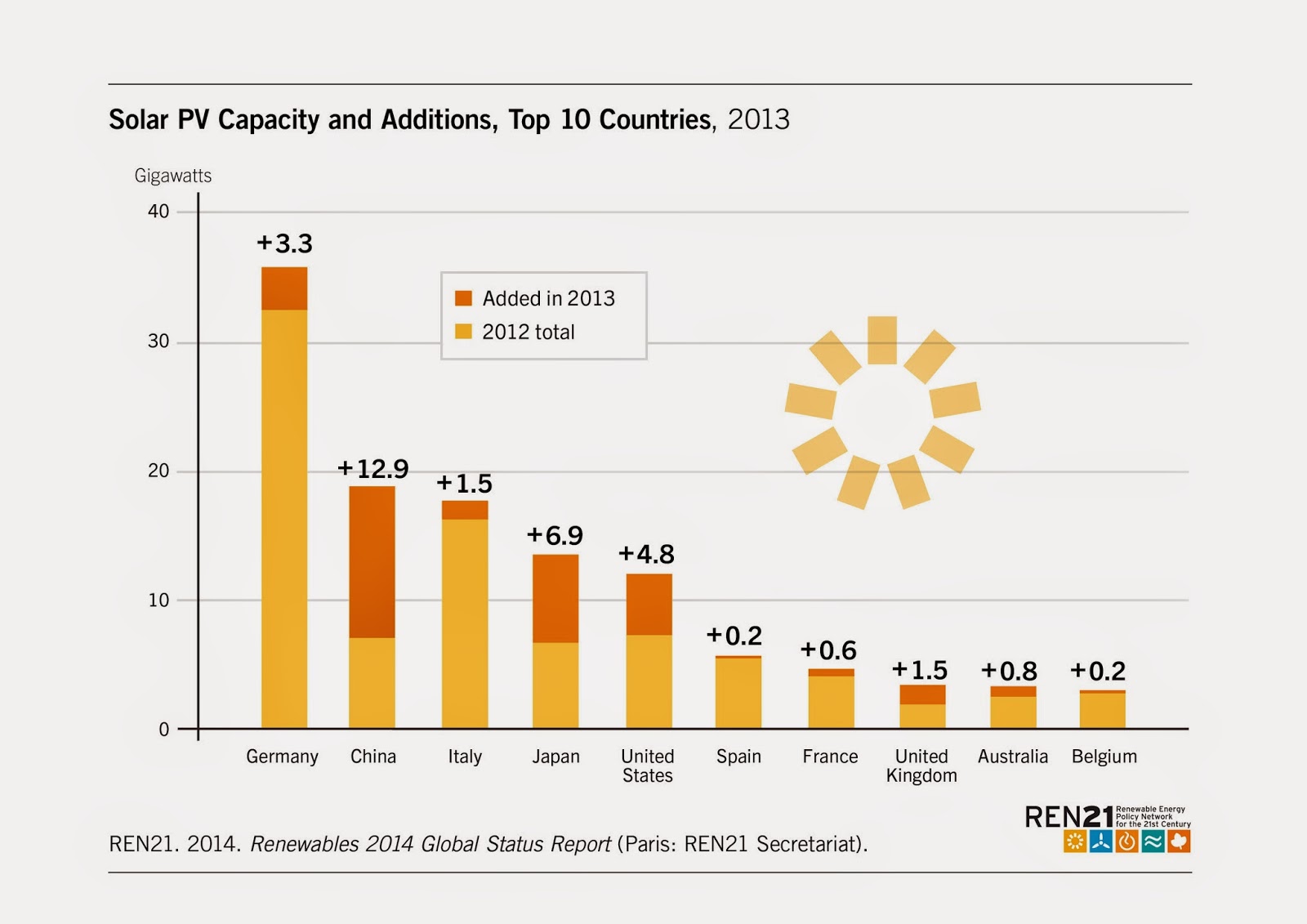

Asia added 22.7 GW to end 2013 with almost 42 GW of solar PV in operation. China alone accounted for almost one-third of global installations, adding a record 12.9 GW to nearly triple its capacity to approximately 20 GW.

Asia added 22.7 GW to end 2013 with almost 42 GW of solar PV in operation. China alone accounted for almost one-third of global installations, adding a record 12.9 GW to nearly triple its capacity to approximately 20 GW.

Capacity has been added so quickly that grid connectivity and curtailment have become challenges. Much of China’s capacity is concentrated in sunny western provinces far from load centers and consists of very large-scale projects, making three state-owned utilities the world’s largest solar asset owners.

Yet there is increasing interest in smaller-scale distributed PV, and the government aims to shift more focus towards the rooftop market.

Japan saw a rush to install capacity in response to its national FIT, adding 6.9 GW in 2013 for a total of 13.6 GW. The majority of Japan’s capacity is in rooftop installations, and homebuilders are promoting solar homes to differentiate their products. For the first time, however, the non-residential sector represented Japan’s largest market. Despite the rise of the large-scale market, many more projects were approved than built in the country due to shortages of land, funds, grid access, qualified

engineers and construction companies, and Japanese-brand equipment.

Japan saw a rush to install capacity in response to its national FIT, adding 6.9 GW in 2013 for a total of 13.6 GW. The majority of Japan’s capacity is in rooftop installations, and homebuilders are promoting solar homes to differentiate their products. For the first time, however, the non-residential sector represented Japan’s largest market. Despite the rise of the large-scale market, many more projects were approved than built in the country due to shortages of land, funds, grid access, qualified

engineers and construction companies, and Japanese-brand equipment.

Elsewhere in Asia, the most significant growth was in India (added 1.1 GW), followed by South Korea (0.4 GW) and Thailand (0.3 GW).

Beyond Asia, about 16.7 GW was added worldwide, primarily in the EU (about 10.4 GW) and North America (5.4 GW), led by the United States—the third largest country-level market in 2013.

U.S. installations were up 41% over 2012 to almost 4.8 GW, for a total of 12.1 GW. Falling prices and innovative financing options that enable installation with low-to-no upfront payment are

changing the game for U.S. consumers.

U.S. installations were up 41% over 2012 to almost 4.8 GW, for a total of 12.1 GW. Falling prices and innovative financing options that enable installation with low-to-no upfront payment are

changing the game for U.S. consumers.

The residential sector experienced the greatest market growth relative to 2012, while large ground-mounted projects represented more than 80% of additions. U.S. businesses made large investments in solar PV to reduce energy costs, and some utility companies signed long-term contracts, choosing solar PV over other options based on price alone. Utility procurement continued to slow, however,

as many approached their Renewable Portfolio Standard (RPS) targets. California installed more than half of the new capacity and is the first major U.S. residential market to successfully transition away from state-level incentives.

Europe continued to operate more solar PV capacity than any other region, with more than 80 GW total by year’s end. But the EU’s 10.4 GW (11 GW in broader Europe) added was less than half the 2011 amount, and the region’s share of the global market also fell rapidly—from 82% in 2010 to 26% in 2013.

In most EU markets, demand contracted due to reductions in policy support and retroactive taxes in some countries, which have hurt investor confidence.

as many approached their Renewable Portfolio Standard (RPS) targets. California installed more than half of the new capacity and is the first major U.S. residential market to successfully transition away from state-level incentives.

Europe continued to operate more solar PV capacity than any other region, with more than 80 GW total by year’s end. But the EU’s 10.4 GW (11 GW in broader Europe) added was less than half the 2011 amount, and the region’s share of the global market also fell rapidly—from 82% in 2010 to 26% in 2013.

In most EU markets, demand contracted due to reductions in policy support and retroactive taxes in some countries, which have hurt investor confidence.

Yet solar PV’s share of generation continues to rise, and PV is increasingly facing barriers such as direct competition with conventional electricity producers. Germany remained the largest EU market, but fell from first to fourth globally, adding 3.3 GW after three years averaging around 7.6 GW. With a total approaching 36 GW, Germany still has the most capacity of any country by far. About one-third of the electricity generated from new systems is used on-site, a trend driven by FIT rates below prices for retail electricity.31 The United Kingdom (adding at least 1.5 GW) emerged as the region’s strongest market for large-scale projects, with subsidies attracting institutional investors and developers from across the EU.

Other top EU markets included Italy (1.5 GW), Romania (1.1 GW), and Greece (1 GW).33 Italy’s market was down dramatically relative to the previous two years, and significant market reductions were seen in Belgium, Denmark, and France.3

Australia installed its one-millionth rooftop system, up from around 8,000 in 2007.35 Over 0.8 GW was added in 2013, as Aussies turned to solar PV to reduce their electricity bills, bringing the total to nearly 3.3 GW. By late 2013, rooftop systems operated on 14% of Australia’s residences, and atop

one-quarter of the homes in South Australia.

In Latin America and the Caribbean, a number of countries had projects in planning or development by year’s end. Markets in Brazil and Chile have been slower to develop than was expected, while Mexico has emerged as a regional leader. Both Chile and Mexico brought several large projects on line in 2013 and early 2014.

Most countries in the Middle East now include solar PV in their energy plans, driven by rapid increases in energy demand, a desire to free up more crude oil for export, and high insolation rates.

one-quarter of the homes in South Australia.

In Latin America and the Caribbean, a number of countries had projects in planning or development by year’s end. Markets in Brazil and Chile have been slower to develop than was expected, while Mexico has emerged as a regional leader. Both Chile and Mexico brought several large projects on line in 2013 and early 2014.

Most countries in the Middle East now include solar PV in their energy plans, driven by rapid increases in energy demand, a desire to free up more crude oil for export, and high insolation rates.

During 2013 and early 2014, large plants were commissioned in several countries—including Jordan, Kuwait, Saudi Arabia, and the United Arab Emirates—and a number of governments signed purchase agreements or launched tenders.

There are also many promising markets across Africa. One of the continent’s largest markets to date is South Africa, which has procured substantial capacity under a government bidding process and connected the first plant (75 MW) to the grid in late 2013.

By early 2014, at least 53 solar PV plants larger than 50 MW were operating in at least 13 countries. The world’s 50 biggest plants reached cumulative capacity exceeding 5.1 GW by the end of 2013. At least 14 of these facilities came on line in 2013, including plants in Japan and South Africa (Africa’s largest).

The largest was a 320 MW PV plant in China, co-located with an existing 1.28 GW hydropower dam. The United States led for total capacity of facilities bigger than 50 MW, with a cumulative 1.4 GW in operation by year’s end, followed by Germany, China, India, and Ukraine.

The largest was a 320 MW PV plant in China, co-located with an existing 1.28 GW hydropower dam. The United States led for total capacity of facilities bigger than 50 MW, with a cumulative 1.4 GW in operation by year’s end, followed by Germany, China, India, and Ukraine.

Many projects are planned and under development around the world that range from 50 MW to over

1,000 MW in scale.

The share of commercial and utility-owned PV continued to increase in 2013, but the residential sector also saw strong capacity growth. Many utilities are pushing back against the expansion of distributed PV in several countries, due to concerns about a shrinking customer base and lost revenue. In Europe, for example, some utilities are blocking self-consumption by instituting fees, raising rates on customers with PV systems, or debating the future of net metering; in several U.S. states, debates are intensifying over net metering laws; in Australia, major utilities are acting to slow or halt the advance of solar PV.

Community-owned PV projects are emerging with a variety of models in an increasing number of countries, including Australia, Japan, the United Kingdom, and Thailand, which has a community solar target under its national FIT. U.S. community solar gardens, which sell power to local utilities in exchange for monthly credits to investors, continued to spread in 2013, and some U.S. states have adopted community solar carve-outs in RPS laws.

1,000 MW in scale.

The share of commercial and utility-owned PV continued to increase in 2013, but the residential sector also saw strong capacity growth. Many utilities are pushing back against the expansion of distributed PV in several countries, due to concerns about a shrinking customer base and lost revenue. In Europe, for example, some utilities are blocking self-consumption by instituting fees, raising rates on customers with PV systems, or debating the future of net metering; in several U.S. states, debates are intensifying over net metering laws; in Australia, major utilities are acting to slow or halt the advance of solar PV.

Community-owned PV projects are emerging with a variety of models in an increasing number of countries, including Australia, Japan, the United Kingdom, and Thailand, which has a community solar target under its national FIT. U.S. community solar gardens, which sell power to local utilities in exchange for monthly credits to investors, continued to spread in 2013, and some U.S. states have adopted community solar carve-outs in RPS laws.

The concentrating PV (CPV) market remains small, but interest is increasing due greatly to higher efficiency levels in locations with high direct normal insolation and low moisture. CPV continued its spread to new markets in 2013, with sizable projects completed in Australia, Italy, and the United States, and small pilots under way in Chile, Namibia, Portugal, Saudi Arabia, and elsewhere. China commissioned the world largest plant (50 MW) during 2013.57 By year’s end, more than 165 MW was operating in more than 20 countries, led by China and the United States.

Solar PV is starting to play a substantial role in electricity generation in some countries, meeting an estimated 7.8% of annual electricity demand in Italy, nearly 6% in Greece, 5% in Germany, and much higher daily peaks in many countries. By year’s end, the EU had enough solar PV capacity to meet an

estimated 3% of total consumption (up from 0.3% in 2008) and 6% of peak demand; global capacity in operation was enough to produce at least 160 TWh of electricity per year.

Solar PV is starting to play a substantial role in electricity generation in some countries, meeting an estimated 7.8% of annual electricity demand in Italy, nearly 6% in Greece, 5% in Germany, and much higher daily peaks in many countries. By year’s end, the EU had enough solar PV capacity to meet an

estimated 3% of total consumption (up from 0.3% in 2008) and 6% of peak demand; global capacity in operation was enough to produce at least 160 TWh of electricity per year.

SOLAR PV INDUSTRY

Following a two-year slump, in which oversupply drove down module prices and many manufacturers reported negative gross margins, the solar PV industry began to recover during 2013. It was still a challenging year, particularly in Europe, where shrinking markets left installers, distributors, and others struggling to stay afloat.

Consolidation continued among manufacturers, but, by late in the year, the strongest companies were selling panels above cost. The rebound did not apply lower down the manufacturing chain, however, particularly for polysilicon makers.

Low module prices also continued to challenge many thin film companies and the concentrating solar

industries, which have struggled to compete. International trade disputes also continued through 2013.

Module prices stabilised, with crystalline silicon module spot prices up about 5% during 2013, in response to robust demand growth in China, Japan, and the United States in the second half of the year.

industries, which have struggled to compete. International trade disputes also continued through 2013.

Module prices stabilised, with crystalline silicon module spot prices up about 5% during 2013, in response to robust demand growth in China, Japan, and the United States in the second half of the year.

At the same time, module production costs continued to fall. Low material costs (particularly for polysilicon) combined with improved manufacturing processes and scale economies have reduced manufacturing costs, and far faster than targeted by the industry, with top Chinese producers approaching costs of USD 0.50/W in 2013.

Interest has turned to lowering soft costs to further reduce installed system costs, which have also declined but not as rapidly as module prices (particularly in Japan and the United States). Although investment in solar PV (in dollar terms) was down for the year, actual installed capacity was up significantly, with the difference explained by declining costs of solar PV systems in recent years.

As of 2013, the cost per MWh of rooftop solar was below retail electricity prices in several countries, including Australia, Brazil, Denmark, Germany, and Italy.

As of 2013, the cost per MWh of rooftop solar was below retail electricity prices in several countries, including Australia, Brazil, Denmark, Germany, and Italy.

By one estimate, solar PV is deemed to be competitive without subsidies in at least 19 markets (in 15 countries). Further, several projects that were planned or under development by year’s end were considered to be competitive with fossil options, without subsidies.

An estimated 43 GW of crystalline silicon cells and 47 GW of modules were produced in 2013, up 20% from 2012, and module production capacity reached an estimated 67.6 GW.

Thin film production rose nearly 21% in 2013, to 4.9 GW, and its share of total global PV production stayed flat year-over-year.

Over the past decade, module production has shifted from the United States, to Japan, to Europe, and back to Asia, with China dominating shipments since 2009.

An estimated 43 GW of crystalline silicon cells and 47 GW of modules were produced in 2013, up 20% from 2012, and module production capacity reached an estimated 67.6 GW.

Thin film production rose nearly 21% in 2013, to 4.9 GW, and its share of total global PV production stayed flat year-over-year.

Over the past decade, module production has shifted from the United States, to Japan, to Europe, and back to Asia, with China dominating shipments since 2009.

By 2013, Asia accounted for 87% of global production (up from 85% in 2012), with China producing 67% of the world total (almost two-thirds in 2012).

Europe’s share continued to fall, to 9% in 2013 (11% in 2012), and Japan’s share remained at 5%. The U.S. share was 2.6%; thin film accounted for 39% of U.S. production, up from 36% in 2012. In India, most manufacturing capacity was idle or operating at low utilisation rates, primarily because it was uncompetitive due to lack of scale, low-cost financing, and underdeveloped supply chains.

Europe’s share continued to fall, to 9% in 2013 (11% in 2012), and Japan’s share remained at 5%. The U.S. share was 2.6%; thin film accounted for 39% of U.S. production, up from 36% in 2012. In India, most manufacturing capacity was idle or operating at low utilisation rates, primarily because it was uncompetitive due to lack of scale, low-cost financing, and underdeveloped supply chains.

Yingli and Trina Solar (both China) were the leading module manufacturers in 2013. They were followed by Canadian Solar (Canada), Jinko Solar, and ReneSola (both China). Sharp Solar (Japan), First Solar (United States), Hanwha SolarOne (China), Kyocera (Japan), and JA Solar (China) rounded out the top 10.

Market consolidation among manufacturers continued in 2013, with merger and acquisition activity reaching record levels mid-year, and bankruptcies and closures continuing.

Market consolidation among manufacturers continued in 2013, with merger and acquisition activity reaching record levels mid-year, and bankruptcies and closures continuing.

CIGSi manufacturers, in particular, faced significant challenges due to standardisation and streamlining of crystalline silicon manufacturing and low silicon prices, with several companies entering insolvency or exiting the industry.

China’s large investment in solar PV manufacturing helped create the supply-demand imbalance that led to industry upheaval, and even China has suffered the results. Much of

the older, less efficient capacity was shut down in 2013, as the national government encouraged consolidation and investment in modern facilities to curb oversupply and to improve quality, which suffered when corners were cut to reduce costs. China’s top 10 companies had more than USD 16 billion in debt by August 2013, and Suntech became the first company ever to default on publicly traded debt in China.

Even as some manufacturers idled production capacity or closed shop, others opened new facilities and began expanding capacity across the globe—from North and South America to Europe, Jordan to Turkey, and Kazakhstan to Malaysia.

Ethiopia’s first module-manufacturing facility (20 MW) began operating in early 2013 to supply the domestic market. Massive new builds were planned in China, which is also set to become a serious thin film player, with Hanergy’s acquisition of several companies in 2013. Japanese manufacturers increased domestic production to meet growing domestic demand.

Innovation and product differentiation have become increasingly important. Successful manufacturers have continued expanding into project development, operations, and maintenance.

China’s large investment in solar PV manufacturing helped create the supply-demand imbalance that led to industry upheaval, and even China has suffered the results. Much of

the older, less efficient capacity was shut down in 2013, as the national government encouraged consolidation and investment in modern facilities to curb oversupply and to improve quality, which suffered when corners were cut to reduce costs. China’s top 10 companies had more than USD 16 billion in debt by August 2013, and Suntech became the first company ever to default on publicly traded debt in China.

Even as some manufacturers idled production capacity or closed shop, others opened new facilities and began expanding capacity across the globe—from North and South America to Europe, Jordan to Turkey, and Kazakhstan to Malaysia.

Ethiopia’s first module-manufacturing facility (20 MW) began operating in early 2013 to supply the domestic market. Massive new builds were planned in China, which is also set to become a serious thin film player, with Hanergy’s acquisition of several companies in 2013. Japanese manufacturers increased domestic production to meet growing domestic demand.

Innovation and product differentiation have become increasingly important. Successful manufacturers have continued expanding into project development, operations, and maintenance.

They also are building strategic partnerships to advance technologies and expand markets. For example, First Solar acquired GE’s cadmium telluride portfolio, while both announced a partnership to advance thin films; SolarCity (United States) teamed up with American Honda and BMW to make solar PV more affordable for hybrid and electric vehicle owners; and Hanergy partnered with retailer IKEA to offer solar PV installation services to U.K. customers.

Manufacturers also joined with utilities and fossil fuel companies to build solar PV plants, while traditional energy and even non-energy companies, such as toll road operator Huabei Express (China), moved further into solar development.

Merger and acquisition activity continued on the development side. Existing large-scale projects were purchased on a far more global scale than in past years, due to increasing ease of financing and growing interest among pure investment firms.

Merger and acquisition activity continued on the development side. Existing large-scale projects were purchased on a far more global scale than in past years, due to increasing ease of financing and growing interest among pure investment firms.

At least two German developers filed for insolvency during 2013, while others expanded their reach—Juwi (Germany) opened a subsidiary in Dubai to serve customers in East Africa and the MENA region.

SunEdison bought EchoFirst (both United States), which offered what it claimed was the first combined solar electric and solar thermal lease for the U.S. residential market.

New business models and innovative financing options continued to emerge, with practices such as solar leasing spreading beyond the United States to Canada, Europe, the Pacific, and elsewhere.

In late 2013, Toshiba (Japan) entered the solar power business in Germany, installing PV systems on apartment buildings and selling electricity to residents directly; systems will be owned and funded by a group of pension funds.

SunEdison bought EchoFirst (both United States), which offered what it claimed was the first combined solar electric and solar thermal lease for the U.S. residential market.

New business models and innovative financing options continued to emerge, with practices such as solar leasing spreading beyond the United States to Canada, Europe, the Pacific, and elsewhere.

In late 2013, Toshiba (Japan) entered the solar power business in Germany, installing PV systems on apartment buildings and selling electricity to residents directly; systems will be owned and funded by a group of pension funds.

By early 2014, Mosaic (United States), an online platform for solar project investments, had financed more than USD 5 million by enabling people to invest small amounts towards specific projects, and SolarCity (United States) announced plans to offer a bond-like product

for individual investors, backed by cash flows from existing customers.

for individual investors, backed by cash flows from existing customers.

New models also are emerging in Latin America, including the sale of PV electricity into the wholesale market (rather than through long-term contracts), with such merchant plants being built in Chile and Mexico.

Solar cell efficiencies continued to increase with more records announced during 2013. Perhaps the biggest technology advance centered on perovskite materials, which experienced a steep rate of efficiency improvement during 2012 and 2013.

They offer the potential for high-performing yet inexpensive solar cells, although they have significant challenges to overcome before coming to market.

CPV had a mixed year in 2013, with key companies closing plants and consolidation affecting both module and system suppliers.

At the same time, the industry saw new strategic partnerships and expansions in manufacturing capacity.

Solar cell efficiencies continued to increase with more records announced during 2013. Perhaps the biggest technology advance centered on perovskite materials, which experienced a steep rate of efficiency improvement during 2012 and 2013.

They offer the potential for high-performing yet inexpensive solar cells, although they have significant challenges to overcome before coming to market.

CPV had a mixed year in 2013, with key companies closing plants and consolidation affecting both module and system suppliers.

At the same time, the industry saw new strategic partnerships and expansions in manufacturing capacity.

Soitec (France) announced plans to consolidate by closing its 40 MW plant in Freiburg, Germany, but also achieved full production capacity at its factory in California, and partnered with Alstom (France) to develop CPV plants in France.

Solar Junction and Amonix (both United States) partnered to improve CPV efficiency.

The industry is showing signs of moving beyond niche markets, with Soitec building a 44 MW project in South Africa, and several companies announcing or commissioning production lines in 2013 to meet growing interest in China.

The industry is showing signs of moving beyond niche markets, with Soitec building a 44 MW project in South Africa, and several companies announcing or commissioning production lines in 2013 to meet growing interest in China.

New cell and module conversion efficiency records were set in 2013, and improvements to mirror and tracker technologies continued.

Solar inverters are becoming more sophisticated to actively support grid management, and are considered one of the fastest developing technologies in power electronics.

Solar inverters are becoming more sophisticated to actively support grid management, and are considered one of the fastest developing technologies in power electronics.

Partly because of this rapid development, in 2013 ABB (Switzerland) acquired Power-One (United States), one of the world’s largest manufacturers of solar power inverters. At the same time, the industry has become increasingly crowded and markets more fragmented, and the largest incumbents faced challenges maintaining growth or even surviving in 2013.

Inverter manufacturers were under pressure to reduce prices, as the European market slowed faster than expected and as the focus of cost-cutting efforts turned increasingly towards balance-ofsystem technologies.